Check requirements for Asia's Retirement Visas

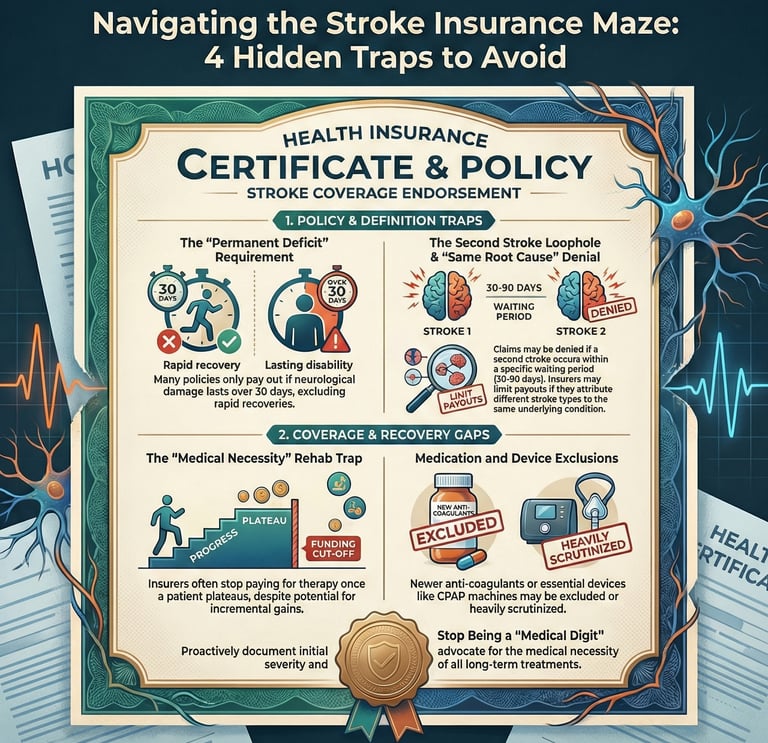

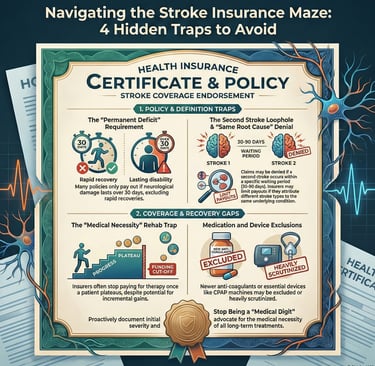

What Are the Hidden Traps in Stroke-Related Insurance Policies?

The Fight After the Fight: Maximizing Your Critical Illness and Health Claims

Surviving a stroke is a medical battle. But often, the next fight—against your own insurance company—is the most frustrating.

After facing two strokes and a mountain of medical bills, I quickly learned that insurance policies are rarely simple safety nets. They are legal contracts loaded with jargon, loopholes, and specific definitions designed to limit their payout. My journey led me to uncover several hidden traps that every stroke survivor and caregiver must know to maximize their claims and access the care they need.

Trap 1: The Critical Illness "Definition Game"

Many people rely on a Critical Illness (CI) rider or policy, which is supposed to pay out a lump sum upon stroke diagnosis. The problem is the definition of "stroke" is often surprisingly strict.

The Fine Print: CI policies frequently define a stroke as requiring permanent neurological deficit for a specific duration (e.g., 30 days) and often demand evidence of necrosis (tissue death) on a scan.

The Consequence: If your recovery is rapid, or if you had a Transient Ischemic Attack (TIA)—which is often called a "mini-stroke" but is a critical warning—the insurer may argue you haven't met the high bar of "permanent damage" and deny the claim. They essentially penalize you for recovering well!

Action Tip: Insist that your neurologist’s documentation clearly records the initial severity of the neurological deficits, regardless of how quickly you recover.

Trap 2: The Second Stroke Loopholes

My situation was complex: a haemorrhagic stroke followed quickly by an ischemic stroke. This is where policies get murky, especially regarding the recurrence rate.

The Waiting Period Trap: Many CI policies have a clause that denies payment for a second CI event if it occurs within a short period (often 30 to 90 days) of the first one, or if it's related to the same underlying cause.

The "Same Cause" Denial: Even if the strokes are different types (bleed vs. clot), the insurer might argue that the underlying high blood pressure or vascular disease is the "same root cause," thus limiting the total payout.

You must review your policy for terms like "Recurrence Clause" or "Waiting Period for Subsequent Claim."

Trap 3: Hidden Limits on Rehabilitation (Rehab)

The most crucial aspect of recovery is often long-term rehabilitation (physiotherapy, occupational therapy). This is where general health insurance policies often drop the ball.

The "Medical Necessity" Trap: Insurers frequently argue that continued rehab is no longer "medically necessary" once a patient plateaus, even if further incremental gains are possible. They will cap the number of sessions allowed per year.

The In-Patient vs. Out-Patient Trap: Policies often provide robust coverage for intensive, in-patient rehab right after the event but offer minimal coverage for the crucial long-term, out-patient sessions needed months or years later.

Trap 4: Medication and Device Exclusion

Policies are constantly updated, and sometimes the newest, most effective medications are not on the preferred formulary.

Specific Drug Denial: If your doctor prescribes a non-generic or a newer, high-cost anti-coagulant, the insurer may reject it, forcing your doctor to switch to a cheaper—but potentially less ideal—alternative.

Durable Medical Equipment (DME) Scrutiny: Devices like the CPAP machine (essential if you have sleep apnea, a major stroke risk) or assistive mobility devices are often subjected to intense scrutiny, requiring precise documentation of medical necessity and often having high co-pays.

The Power of Documentation and Advocacy

Dealing with insurance requires you to stop being a passive "medical digit" and become an active advocate. 保险—insurance—should be your shield, not your enemy.

The financial stress of a health crisis can severely impede recovery. Arm yourself with knowledge of these traps. Your recovery depends not only on your diet and exercise but also on your ability to secure the financial resources for your long-term health.

Have you fought an insurance denial? Share your number one tip for winning an appeal to help others!

Find out about the day I had my stroke:

https://www.eatruntravelretire.com/true-story-a-stroke-survivor

Find out how I had a second stroke and survived again! https://www.eatruntravelretire.com/what-is-the-risk-of-a-second-stroke

Find out how I change my diet and lifestyle: https://www.eatruntravelretire.com/eating-right-diet-after-a-stroke

Disclaimer: I am sharing my personal journey as a stroke survivor only and does not constitute professional financial or legal advice. Always consult with a licensed insurance advisor or financial professional regarding your specific policy details.

Address

Blk 8 Cantonment Close

SIngapore